(Bloomberg) -- The US Treasury is expected to make its fourth straight reduction in a quarterly sale of longer-term debt this month, with most dealers predicting extra cutbacks for the 20-year bond.

The Treasury on Wednesday will announce its so-called quarterly refunding auction, and dealers expect a fourth straight reduction in total issuance -- the longest such string in about eight years. That’s seen giving the department room to ramp up sales of Treasury bills, which have been in big demand as investors have flocked to short-dated instruments amid economic uncertainty.

In its broader announcement on debt issuance over the coming quarter, many dealers predict the Treasury will put extra weight on trimming back sales of the 20-year bond, which was reintroduced two years ago but has proved more costly than either 10-year or 30-year Treasuries. Yields on the 20-year Treasury fell as much as 10 basis points on Monday, outperforming other maturities, after several dealers predicted larger auction size cuts for that tenor than those made in May.

“The problem child in the Treasury’s auction line-up” is how Lou Crandall at Wrightson ICAP LLC terms the 20-year bond. While he had criticized the Treasury’s abandonment of the 20-year back in 1986, today he highlights that its resurrection hasn’t won backing from the market.

Most dealers see the refunding, which spans 3-year, 10-year and 30-year securities, totaling $98 billion, down from the $103 billion sold in May. Record revenues -- stoked in part by strong wage gains in the current high-inflation economy -- have given the Treasury space to trim its borrowing.

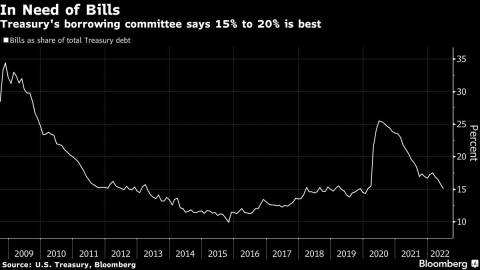

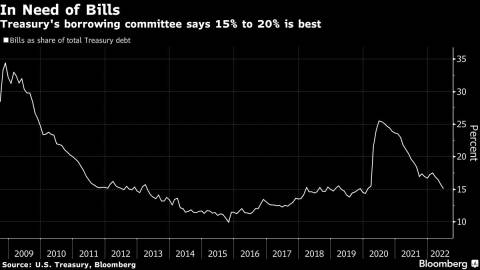

Bill Demand

In the run-up to the refunding, the department queried dealers on the low levels of T-bills in the marketplace. That bolstered expectations for a potential expansion in bill sales as the Treasury trims coupons, or interest-bearing securities.

“There’s a need for more Treasury bills, so another round of coupon-cuts is required,” said Michael Cloherty, head of US rates strategy at UBS Group AG. “Given the growth of the money-fund industry over recent years, it’s appropriate for the percentage of T-bills to be even higher than it used to be” as a share of overall federal debt, he said.

As for coupons, the Treasury has made larger reductions to the 20-year bond along with seven-year notes in recent quarters. There is some disagreement among dealers over just which tenors are likely to be cut this time around, and by how much.

- HSBC Holdings Inc. and Nomura Securities both see cuts of $1 billion per month to sales of 2-, 3-, 5- and 7-year debt over the coming quarter and similar-sized trimmings to new-issue and reopening sales of 10- and 30-year securities. For the 20-year, they predict a $3 billion cut to new-issue and reopening auctions

- Societe Generale, Citigroup Inc. and RBC Capital see similar reductions, except the outsized trimming of the 20-year is only on the order of $2 billion at each sale

- UBS Group AG and Bank of America Corp. for their part are closely in line, except they see heavier cuts to both 7-year and 20-year debt

- Goldman Sachs Group Inc. sees only reductions to the 5-year, 7-year and 20-year maturities

- While Deutsche Bank AG forecasts reductions for just the 7-year and 20-year tenors

Dealers generally agree that sales of Treasury Inflation-Protected Securities, known as TIPS, are likely to be increased again. The government has been trying to increase TIPS as a share of the outstanding debt over time.

What’s been sinking as a share is T-bills. The Treasury Borrowing Advisory Committee, a group comprising dealers, investors and other stakeholders, has several times in the past advised that bills amount to about 15% to 20% of the total debt pile. The ratio is at the bottom of that range now.

Read More: Goldman Sees Imminent End to ‘Uncomfortably Low’ Bill Supply

On Monday, the US Treasury lifted its estimate of federal borrowing for the three months through September as it took into account the Fed’s balance sheet runoff and adjusted for change in fiscal activity. It left the cash balance target steady at $650 billion for the end of the period; it’s currently under that level.

Quarterly refundings soared to a record $126 billion by February 2021 from $84 billion on the eve of the pandemic. After several quarters of cutbacks, the Treasury at some point is expected to hold the sales steady, or even boost them again, as the Federal Reserve shrinks its bond portfolio -- forcing the Treasury to borrow more from the public.

“Looking into 2023 and 2024, that will reverse,” Steven Zeng, a rates strategist at Deutsche Bank AG, said of the Treasury’s current over-financing.

But that dynamic isn’t yet in play.

“The upcoming refunding is going to be focused on further reduction in issuance based on an improving fiscal landscape and in spite of higher anticipated funding needs stemming from” the Fed’s shrinking portfolio, Jefferies economists Thomas Simons and Aneta Markowska wrote in a note.

(Adds details from Treasury’s financing estimates released Monday.)

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.

Author: Liz Capo McCormick